For Canadian income investors seeking stable returns, Guaranteed Investment Certificates (GICs) have long been a cornerstone. Their simplicity and principal protection offer a comforting sense of security. However, as investors increasingly look beyond traditional instruments for enhanced yield and diversification, a compelling alternative in the private credit space has emerged: Mortgage Investment Corporations (MICs). Yield the North believes this shift is not merely a search for higher returns, but a strategic alignment with the most structurally stable segment of Canadian commercial real estate, multifamily and affordable housing, underpinned by robust fundamentals and unparalleled government-backed financing.

The Allure of Predictable Income: Redefining Fixed Income

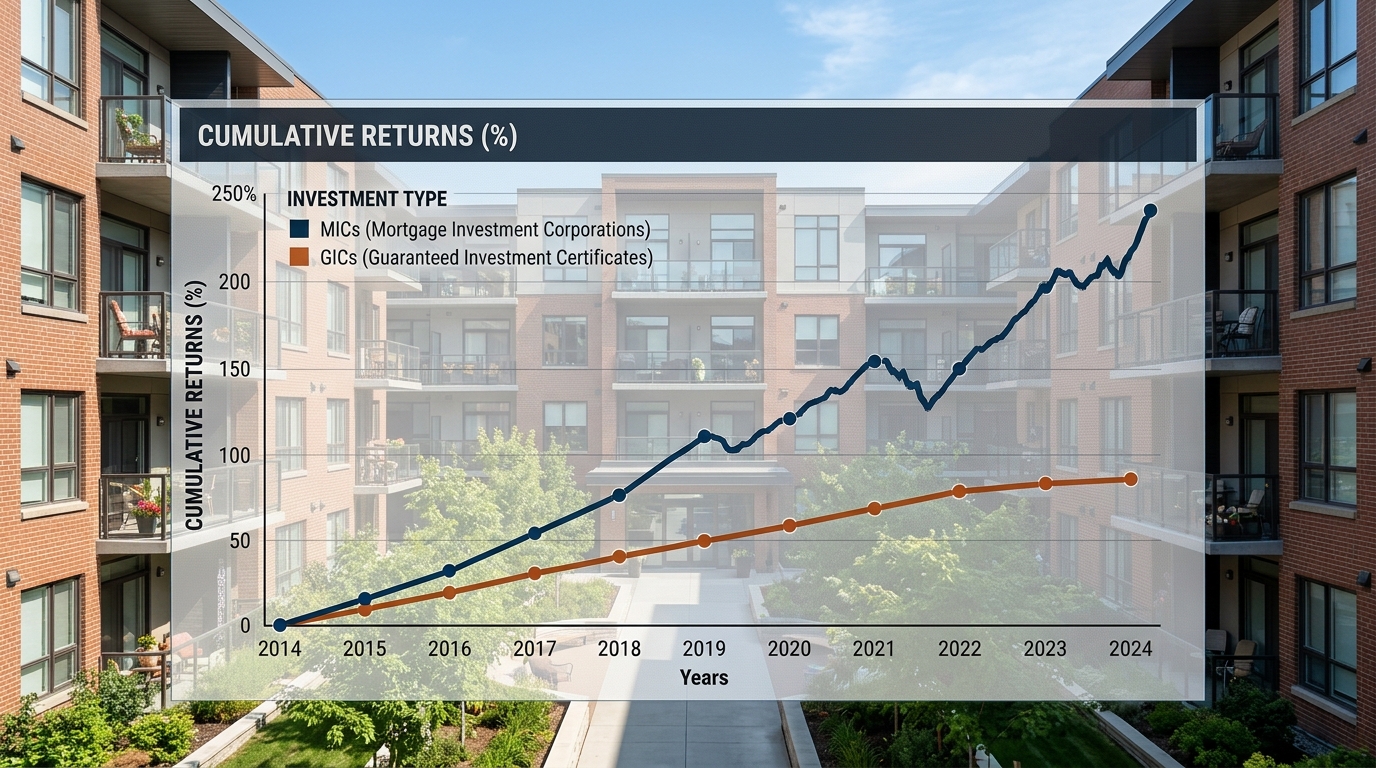

Traditional fixed income investments, like GICs, remain popular for their low risk profile and predictable interest payments. In the current economic climate, GIC rates have offered a respectable, albeit modest, return, typically ranging from 4% to 5% for terms between one and five years. While this provides capital preservation, it often struggles to keep pace with inflation or generate substantial wealth growth, particularly after taxes. For income-focused investors, the search for yield that genuinely contributes to portfolio growth and income generation has become paramount. This quest naturally leads to the private credit market, where Mortgage Investment Corporations offer a distinct advantage.

MICs are investment vehicles that pool capital from investors to provide mortgage financing, primarily to borrowers who may not meet the strict underwriting criteria of traditional banks, or who require specialized financing solutions. These can include construction loans, bridge financing, or mortgages on unique properties. Crucially, a significant portion of MIC lending is directed towards income-generating real estate, including multifamily and affordable housing projects, aligning directly with Yield the North's core investment thesis. These private mortgages often command higher interest rates than conventional bank loans, translating into superior yields for MIC investors, commonly in the range of 8% to 12% annually, before fees.

Mortgage Investment Corporations: Fueling Canada's Housing Ecosystem

Canada's MIC sector has seen significant expansion, reflecting a growing need for alternative financing in the real estate market. Firms like Gentai Capital, recognized for their growth and alternative mortgage solutions, exemplify the dynamism within this sector. MICs play a vital role in bridging the financing gap, particularly for projects that contribute to Canada's housing supply, including purpose-built rental and affordable housing developments. This private capital complements traditional lending, ensuring that critical housing projects can move forward.

Unlike publicly traded entities such as Atrium Mortgage Investment Corporation, which operates on public exchanges and recently announced a Normal Course Issuer Bid, many MICs operate within the exempt market, providing direct access to private real estate credit opportunities. This private market exposure allows investors to bypass the volatility often associated with public markets, investing directly in income-producing real estate debt. The underlying assets, particularly multifamily and affordable housing, benefit from persistent demand driven by Canada's aggressive immigration targets, aiming for over 500,000 new permanent residents annually by 2026, and continuous household formation. This structural demand ensures a stable revenue floor for these properties, making the mortgages backed by them inherently robust.

Yield, Liquidity, and Risk: The MIC-GIC Trade-Off

For income investors, the decision between a GIC and a MIC boils down to a fundamental trade-off between yield, liquidity, and risk. GICs offer high liquidity and virtually no principal risk, but commensurately lower yields. MICs, by their nature as private investments, offer significantly higher yields but come with reduced liquidity. This means that capital invested in a MIC may not be as readily accessible as funds held in a GIC.

The Globe and Mail recently highlighted instances where mortgage lenders temporarily halted investor redemptions in residential real estate funds. This underscores the importance of understanding the redemption policies of any MIC investment. Unlike GICs, which have fixed terms and guaranteed payouts, MICs typically offer redemptions on a quarterly or semi-annual basis, often subject to notice periods and the fund's liquidity position. While this characteristic demands a longer-term investment horizon, it is a known attribute of private market investments, not an unforeseen challenge. The higher yields offered by MICs are, in part, compensation for this reduced liquidity and the active management of a mortgage portfolio. For investors with a portion of their portfolio allocated for longer-term income generation, the illiquidity of MICs is a manageable characteristic, not a deterrent.

Furthermore, the risk profile of MICs is tied to the quality of their underlying mortgage portfolios. Disciplined lending, as highlighted by mpamag.com, is crucial for success in the MIC sector. Investors must perform due diligence on the MIC's management team, underwriting standards, loan-to-value ratios, and geographic focus. Yield the North's emphasis on Ontario's secondary markets and the multifamily segment provides an additional layer of confidence, as these areas often present strong demographics and less speculative market dynamics compared to some primary urban centers.

CMHC MLI Select: A Pillar of Stability for Private Credit

One of the most compelling aspects bolstering the stability of Canadian multifamily real estate, and by extension, the private credit ecosystem that finances it, is the Canada Mortgage and Housing Corporation's (CMHC) MLI Select program. This program offers highly attractive financing terms for purpose-built rental and affordable housing projects, including loan-to-value ratios of up to 95% and amortizations extending to 50 years. No other asset class in Canada benefits from comparable government-backed financing, making it an exceptionally efficient deployment of capital.

While MICs directly provide private credit, the presence and popularity of CMHC MLI Select financing indirectly enhance the stability and attractiveness of the entire multifamily lending landscape. Projects that qualify for MLI Select benefit from lower borrowing costs and extended amortization periods, which improve their long-term viability and cash flow. This creates a more robust environment for all lenders, including MICs, by ensuring a strong, well-financed pipeline of projects that meet critical housing needs. CMHC's ongoing refinement of its programs, such as the recent setting of new operating expense benchmarks for MLI Select, demonstrates its active role in shaping a sustainable and transparent lending environment.

Affordable housing, in particular, sits at the intersection of structural demand, regulatory support, and efficient financing. It is often the focus of MICs seeking stable, impact-driven returns. The combination of strong rental demand, rent control protections that establish a revenue floor, and the unique advantages of CMHC MLI Select financing makes affordable housing the safest investable segment in Canadian real estate today. Private credit, through MICs, provides essential funding for this segment, allowing investors to participate in this stability.

Strategic Allocation: Private Credit in a Diversified Portfolio

For investors looking to optimize their portfolio for income, allocating a portion of capital to private credit through MICs represents a strategic move. It offers diversification away from traditional equities and bonds, provides exposure to real assets, and captures a premium for the illiquidity inherent in private markets. This type of private investing allows income investors to tap into the resilient Canadian real estate market, particularly the multifamily and affordable housing sectors, which are insulated from discretionary consumption patterns.

The structural supply gap for housing across Canada is not closing. CMHC has estimated that 3.5 million additional housing units are needed by 2030 to restore affordability. This persistent imbalance between supply and demand ensures that rental housing, especially purpose-built and affordable units, will remain a high-demand asset class. Private credit, facilitated by MICs, is a critical component in financing the construction and acquisition of these essential properties, providing investors with a direct pathway to participate in this enduring market dynamic.

Conclusion: The Enduring Signal of Canadian Multifamily Private Credit

Yield the North maintains its unwavering belief in the Canadian real estate market, with multifamily and affordable housing as its structurally stable core. While asking-rent volatility or market corrections may generate headlines, the true signal for investors lies in in-place revenue, persistent structural demand, and the unparalleled efficiency of CMHC MLI Select financing. Mortgage Investment Corporations offer income investors a compelling alternative to traditional GICs, providing access to superior yields by channeling capital into the robust Canadian multifamily sector.

By understanding the yield-liquidity trade-off and focusing on disciplined MICs with strong underwriting, investors can unlock significant income potential. Private credit is not merely an alternative; it is an essential engine fueling Canada's housing supply and an increasingly vital component of a well-diversified, income-generating portfolio, grounded in the unshakeable fundamentals of Canadian housing demand.